Bitcoin

“Bitcoin has huge potential in Africa.” – An Interview With BitHub Africa’s John Karanja

On the 25th of August, I had the pleasure to interview BitHub Africa‘s founder John Karanja in his office in Nairobi. During our conversation, we discussed the potential and the challenges of bitcoin adoption in Kenya and Africa.

BitcoinAfrica.io: How do you see the current situation for bitcoin in Kenya and Africa in general?

John Karanja: I think bitcoin is still in the early stages, even beyond Africa. In Kenya, we see bitcoin adoption is mainly with speculators and traders who are buying and selling bitcoin to make money. Volumes have been growing over time. I think it’s about 10 million shillings weekly, which is around $100,000 traded every week on the peer-to-peer platform LocalBitcoins.com.

BitcoinAfrica.io: Is LocalBitcoins the main exchange used in Kenya?

John Karanja: Yes, it is. Bitcoin in Kenya is still are a very early stage. There are start-ups that have come and gone because it appears that bitcoin is not ready to scale amongst the average person here. Hence, it’s not going to compete with the mobile money system M-Pesa, for example, at least in the short term.

I think what we’re seeing is now more focus shifting to blockchain technology, being used in other use cases like identification systems, data storage or smart energy. We’re applying ourselves in these different areas to see which are the most viable and we will then launch our projects after doing so. In fact, we’ve produced a report on blockchain opportunities in Africa that goes into depth on that subject. The report, titled The African Blockchain Opportunity, was officially launched at the AITEC Summit in Nairobi on the 31st of August. The reason we produced the report is to provide the information about the potential opportunities that the blockchain technology is creating in Africa for entrepreneurs.

That’s where we are at the moment. We’ll probably launch our first project in early 2017 using the blockchain. So far, our work has primarily been focused on research and development here at BitHub.

BitcoinAfrica.io: To touch on the point you made about the move away from bitcoin to the blockchain. Do you think that, while the initial bitcoin in Africa story was remittance and supporting the underbanked population, there is a move away from that to a focus on the blockchain for commercial users as it very much is in the Western world now?

![]() John Karanja: I’d say they’d go in parallel because bitcoin has a lot of inherent advantages over any other secondary blockchain platform, in that it’s the most secure, it has the largest user base, it has a lot of liquidity and there’s money going in. But in terms of the user experience, it’s not quite mature yet. However, there are a lot of people working on improving that. So I think that will eventually be resolved but the technology is so disruptive that it can be applied to so many areas, some of which are fairly simple like storage of data, for many small enterprises getting cloud systems or complying with KYC. For these types of systems, the cost is often quite prohibitive. So what the blockchain can do is streamline that and open access to everyone. Identifying a customer, then also supplying him the products and enabling payment. So the blockchain can cover that whole process from start to finish. I see both bitcoin and the blockchain moving together.

John Karanja: I’d say they’d go in parallel because bitcoin has a lot of inherent advantages over any other secondary blockchain platform, in that it’s the most secure, it has the largest user base, it has a lot of liquidity and there’s money going in. But in terms of the user experience, it’s not quite mature yet. However, there are a lot of people working on improving that. So I think that will eventually be resolved but the technology is so disruptive that it can be applied to so many areas, some of which are fairly simple like storage of data, for many small enterprises getting cloud systems or complying with KYC. For these types of systems, the cost is often quite prohibitive. So what the blockchain can do is streamline that and open access to everyone. Identifying a customer, then also supplying him the products and enabling payment. So the blockchain can cover that whole process from start to finish. I see both bitcoin and the blockchain moving together.

BitcoinAfrica.io: Do you think bitcoin remittances will still be a growth market in Africa? One thing that you have now is there are so many low-cost remittances services, such as World Remit, TransferWise and CurrencyFair. Do you think that because of them, bitcoin for remittances is not going to be such a big growth market anymore as the cost of exchanging bitcoin back into local African currency can be quite high at times when using peer-to-peer exchanges as Citigroup pointed out in a recent research piece?

John Karanja: Bitcoin is not the clear winner yet when it comes to remittances. However, it is very much a possibility that it will be integrated into the background. For example, WorldRemit could end up using it for settlements, rather than pushing customers to use bitcoin. And we shouldn’t forget that there is still huge risk associated with bitcoin as its infrastructure is still relatively underdeveloped.

At the end of the day, it’s a protocol, it’s not an application. I don’t think anyone can say for sure bitcoin is dying or Bitcoin will succeed. But there’s also the possibility that we’ll see better technology rising very quickly and learning from what Bitcoin has been able to achieve.

BitcoinAfrica.io: Aside from Kenya, Nigeria, Ghana and South Africa, which country do you think will be the next African country to witness a reasonable rate of bitcoin adoption and the growth of a local bitcoin ecosystem?

John Karanja: I think those are the main countries. Possibly we could also see Rwanda because Rwanda has a very aggressive education platform that is aiming to leverage technology. I think that’s one country that’s usually left out, but it’s mostly those countries that have already advanced in terms of the internet and social media adoption. You can just look at Facebook statistics and see the countries where Facebook is heavily adopted. Those will be the likely next adopters of Bitcoin.

BitcoinAfrica.io: I read about how the telecoms giant Safaricom banned Bitcoin on their mobile money platform MPESA. Do you think that the “Safaricoms” in the other African countries will also try to hinder Bitcoin innovation to prevent their mobile payments systems from disruption?

John Karanja: That’s a good question. I’d say right now, ironically, more Bitcoin is traded using M-Pesa than ever before because of LocalBitcoins. They wouldn’t really be able to stomp it out but what they’d be able to do is restrict other centralized entities from using bitcoin as a platform to scale because obviously, they would be potential competition to them.

There may be room for telecoms innovating using bitcoin, but that would be very risky because bitcoin and other cryptocurrencies seem to work best in a peer-to-peer format because the risk is distributed as much as possible. If I’m sending you Bitcoin you send me M-Pesa, it’s just me and you. The counterparty risk is between me and you. It’s not in a centralized place that can get hacked. My guess would be that peer-to-peer platforms are where Bitcoin would dominate.

I don’t know if you saw the President signed the law that caps the interest rates at 14%?

BitcoinAfrica.io: Yes. I read that.

John Karanja: That’s the kind of situation that can now allow for bitcoin to triumph because the banks will not be too interested in micro-lending and may wish to partner with fintech solution providers to provide liquidity in that market segment. Therefore, people will now move more towards peer-to-peer or social lending platforms. I think in a peer-to-peer world bitcoin could dominate. The question is how simple can the peer-to-peer applications become? Because the peer-to-peer ecosystem is not really developed enough to be a safe and secure way to transact in digital currencies.

BitcoinAfrica.io: What are your thoughts on Ethereum and what do you think about ether from an investment point of view?

John Karanja: We did a study on it. It’s in the report. I believe Ethereum will have much more challenges than Bitcoin because they’ve used a high-level computer programming language called Solidity that essentially allows you to program ‘what if’ statement. But now, as they’ve realized from the Dao attack, by doing so that they opened so many vulnerabilities for attacks. For them to plug that, as a developer, I see that being more difficult than using a low-level platform like bitcoin where the rules are fixed. There are few rules and they are fixed. On the bitcoin platform, there’s no variation on what can happen. We know what can happen on that platform.

Ethereum, I would call ambitious but the advantage they have is they are secure. They have a good amount of miners behind the network. They’ve managed to attract enough interest in terms of safeguarding and keeping the platform that if they figure out their niche, it could advance blockchain technology even further.

BitcoinAfrica.io: My last question is about The African Blockchain Opportunity report that you have published. You mentioned it briefly earlier. Could you elaborate on it, please?

John Karanja: Essentially the whole idea behind the report is to provide a manual that anyone can pick up, whether it’s a developer, a bitcoin enthusiast or an entrepreneur and read up on areas of interest. It covers the technical aspects of bitcoin and the blockchain technology within an African context.

There are also a couple of chapters on fintech and we also have linked several developer resources. A developer can go and look at the source code and then try to either contribute or fork it and develop it as an application. We’re now going to be using that for our training curriculum. Then hopefully the idea is to have a second edition maybe in one or two years from now with updates.

BitcoinAfrica.io: Thank you for taking the time to conduct this interview.

BitcoinAfrica.io: Thank you for taking the time to conduct this interview.

If you want to find out more about BitHub Africa visit their website and if you would like to purchase the report The African Blockchain Opportunity click here or on the banner on the right. If you would like to reach out to John directly, you can find him on Twitter at @BitHubAfrica.

Statistics, examples, and ways to legally use cryptocurrency

October 1, 2013, was a turbulent day for San Francisco Public Library. A dozen FBI agents pretending to be usual visitors surrounded a man sitting at one of the tables, took his laptop and put a pair of handcuffs on his hands. That man was Ross Ulbricht, founder of Silk Road – the largest darknet marketplace for drug dealers, killers, and other criminals. The seizure of Ulbricht was supposed to tackle the illegal online trade, but, as the news site DeepDotWeb wrote, the bust was “the best advertising the darknet markets could have hoped for”. The reputation of cryptocurrency also suffers from associations with terrorists, who sometimes use it for their needs. How big is the real scale of the problem? And how many legal ways to use crypto exist? ChangeNOW has dived into the topic – and suggests you an overview of the current state of the problem.

Highlights:

- The drugs trade volume using cryptocurrency is relatively large

- Crypto was a significant reason why a part of drug sales migrated to the web, though stays yet not viable and anonymous enough for dealers (same as for terrorists)

- As efficient use of blockchain technology requires good infrastructure, crypto remains not suitable enough for many terrorist groups

- However, some terrorists are trying to adjust to anonymity threats and hold fundraising in crypto

- Legal ways to use cryptocurrency include dozens and vary from IT services to car rentals

Crypto & Drugs & Rock’n’Roll

The total volume of the online drug market using cryptocurrency is around $1 billion. It is located in the darknet, which provides an attractive, profitable, and mostly secure environment for drug dealers. Cryptocurrency, in turn, allows making payments that are hard to be tracked by authorities. This is how blockchain technology has helped to bring a big part of drug sales online from the streets. And it’s not only about drugs themselves – many legal opioid drugs are illegally sold here, too.

However, cryptocurrency is not always as secure and anonymous as it is thought to be. The information about any transaction ever made stays forever in the blockchain, which makes the system way more transparent than cash payments. This is a significant limitation for using crypto in illegal purposes.

According to the University of Technology Sydney, about 46% of criminal activity of each year is connected to Bitcoin. As for the drug sale itself, trade volumes in crypto keep rising, but the percent of Bitcoin drug transactions out of all transactions goes down. This means Bitcoin is more frequently used for legitimate purposes.

What cryptocurrency is used for drug sales most often? Surprisingly, privacy coins such as Monero are used only for 4% of transactions. Due to its pioneer position, Bitcoin is used in 76% of all deals despite all its anonymity risks.

The main problem for drug dealers using crypto is to turn their income into cash. This move remains complicated and insecure. Most cryptocurrency exchanges have instruments to define whether a transaction is coming from a suspicious source like the darknet. The rise of Monero use in the online drug market will hinder such tracking. However, for the reasons listed above, crypto is unlikely to completely replace regular cash in drug sales in the foreseeable future.

Cryptoterrorism

The views on how much cryptocurrency is used and will be used by terrorists vary widely. While some claim that terrorists have no infrastructure to use it and the methods are not secure enough, others argue that they are learning fast and adjust to crypto rapidly. Let’s see what both sides say.

Not actively using, unclear future

Lack of appropriate infrastructure, inability to use crypto. Most terrorist groups settle in the Middle East region, especially on its remote and war-torn territories. The vast majority of roads and technological infrastructure have been destroyed. In such circumstances, cash remains the most common and convenient way to pay and fundraise. Imagine a gun seller in a Syrian village – does it look like he has a tool to accept Monero?

Anonymity threats. Given the relative transparency of blockchain mentioned above, crypto might remain too unsafe for terrorists. Miners can see any potential terrorist money exchange while checking transactions, and it’s not too hard to see who sends them money. It can change with the rising use rate of privacy coins, but the ability to spend such money remains questionable.

Increased attention to crypto by the authorities. As the number of transactions keeps rising, more regulatory bodies’ attention gets focused on cryptocurrency, which apparently makes terrorists nervous and cautious.

Problems of specific currencies. While top cryptocurrencies like Bitcoin receive much regulatory attention, others remain marginal and unreliable because of a lack of support. Conflicts and uncertainty lower the trust to such cryptocurrencies – yes, even terrorists’ trust.

Using actively now, increasingly in the future

Terrorists seem to be rapidly learning to escape from tracking in blockchain. Several years ago it was easy to find any address or transaction made for a terrorists’ fundraiser. Today they use well organized and finely designed websites, where detailed video tutorials show how to donate money anonymously. Unique Bitcoin addresses and other crypto tricks are used to preserve security. Analysts from intelligence services claim there’s only going to be more such cases. And, of course, privacy coins are a “great opportunity” for terrorists too.

Shift to cryptocurrency is a reaction to economic sanctions. ISIS has lost most of its territory and resources, Hamas has been sanctioned by the West. Having been cut off from all main financial institutes, terrorist groups had to find other pathways for their financial activities – and cryptocurrency appeared to be the best substitute.

There might be difficulties and inconveniences, and the number of terrorists using crypto is yet unknown – but as we can see, digital money in terrorism is reality. Same as in drugs. And this is what cryptocurrency is notorious for, lacking trust among millions of people. The reputation of some of the exchange services only adds to this mistrust – ChangeNOW has carried out a special investigation on how such platforms may cheat their clients. But can you buy anything besides heroin and firearms with your crypto? What about pizza or a concert ticket?

Only Antarctica left

Cryptwerk, a platform monitoring actual use cases of different cryptocurrencies, says there are about 3500 ways to spend Bitcoin and more than 800 for Monero today. They range from music services to car rentals, from buying clothes to hotel booking services, and from sports bets to virtual tours.

Organizations accepting cryptocurrency are located on all continents besides Antarctica (what could be a better place for crypto than a continent without governments and countries though?). Mostly, in the USA and Central Europe. Bitcoin as the largest cryptocurrency is relatively widespread in India and Southeast Asia.

As this is a whole another topic, ChangeNOW will issue a post dedicated to use cases of cryptocurrencies. As it will be more detailed, who knows – maybe you’ll find a pizza right by that you could pay for from your crypto wallet!

This article was contributed by Jeremy from ChangeNow.

Magic Eden Has Quietly Become the Best Ethereum NFT Marketplace

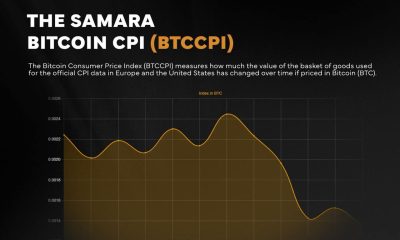

Samara Asset Group Launches Bitcoin CPI (BTCCPI)

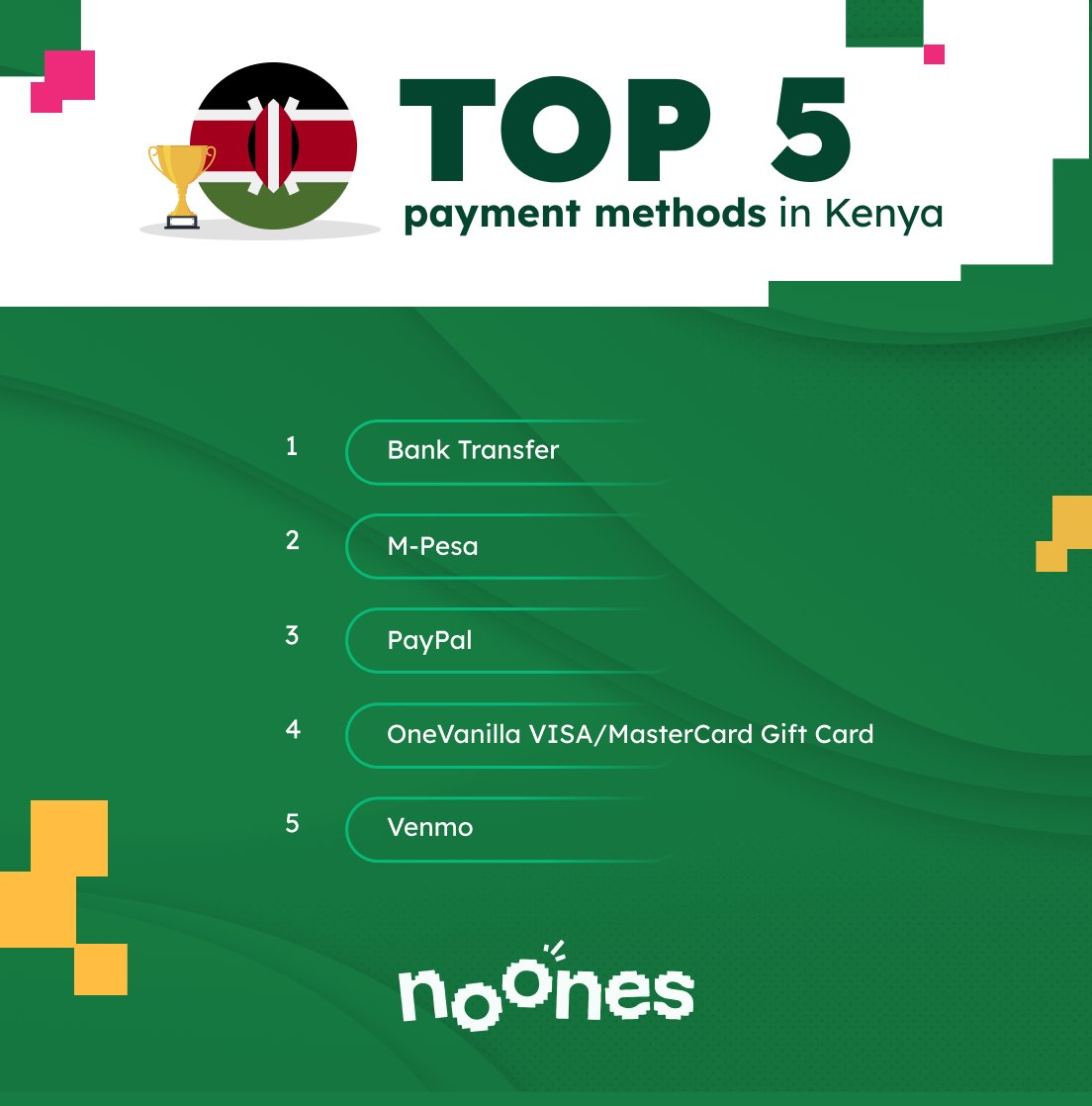

Introducing Noones – Africa’s P2P Super App

Why Crypto’s Leading the Way in Africa’s Evolving Finance Landscape

The Rise of Bitcoin in the Online Gaming World

Unlock the Thrills of NHL Crypto Betting and Live Streaming

Understanding the Impact of Cryptocurrency Volatility on NBA Betting Markets

The Future of Crypto College Football Betting: Trends and Predictions

How Mobile Apps are Changing Sports Betting