Features

How FinTech Companies Changed Africa

Although Africa’s economies may be lagging behind its more developed counterparts, it seems that the continent is not immune to the global fintech revolution. Africa started witnessing a substantial surge in fintech startups in 2015. The total funding from venture capitalists spiked by 51 percent to $195 million between 2016 and 2017, with fintech funding accounting for a third of the amount. That’s a significant amount given that total global funding for seed-stage companies, early-stage venture capitalist rounds, and VC rounds was $851 million, $7.137 billion, and $6.9 billion respectively.

Currently, there are well over 300 startups in operation all over the continent — 94 operate in South Africa, 74 in Nigeria, and 56 in Kenya. It’s not a surprise that these three countries are spearheading the fintech revolution in Africa as they are considered the top three investment destinations in Africa.

Regional comparisons in fintech adoption show that South Africa is in the lead with around 35 percent of fintech startups concentrated in the region. West Africa follows close behind with around 34 percent.

Africa’sfintech industry to a large extent owes its existence to the development of M-Pesa, a Kenyan-based mobile money transfer service that has given Kenyans the ability to access financial services away from banks. Currently, the platform supports over 25 million customers in over ten markets in Europe, Africa, and Asia. The number of M-Pesa users has grown by 32 percent from 17.12 million to 22.62 million as of June 2017. The massive success enjoyed by M-Pesa has influenced other FinTech companies to join the finance sector to develop financial solutions such as those offered by M-Pesa.

Fintech Implementation in Africa

Fintech companies in Africa are mostly focusing on two broad categories:

- payments and transfers;

- lending and finance.

Of the two categories, payments and transfers have recorded an influx of startup companies compared to the others. Reports show that a majority of these startups focus mainly on simplifying the process of sending and receiving money.

Some fintech companies in Africa that are taking major steps in revolutionising the finance sector in Africa include (aside from M-Pesa):

- Flutterwave has operations in over 36 countries and is partnered with 10 African banks. It provides payment technologies and infrastructure to Africa’s largest financial institutions. Today, Flutterwave has processed over $1.2 billion in payments. The primary goal of Flutterwave is to provide solutions for enterprises, entrepreneurs, and banks alike. It presents its customers with no special, annual, or upfront project fees. Instead, Flutterwave bridges the digital payments gap that exists between users and banks. Their Nigerian customers can execute money transfers directly into several bank accounts without any hassle.

- Pezesha, initially launched in Kenya, is a peer-to-business micro-lending marketplace made up of low-income borrowers. In Africa, formal credit services are hard to attain, and on top of that, they have incredibly high interest rates. Therefore, most Africans are unable to secure reliable credit facilities that they can safely payback. Users of Pezesha can acquire instant loans on their mobile phones via SMS provided that minimum criteria are met. Apart from low-income earners, Pezesha also extends its services to SMEs that make up 80 percent of Africa’s employment. It not only drives up the economies of the continent but ensures the continued existence of small businesses across the continent.

- Cellulant, a digital commerce and payments service provider, is well established and operational in 11 countries. The company works with over 90 banks. The Cellulant ecosystem has support for over 100 million customers. As of January last year, the company served roughly 12 percent of Africa’s mobile consumers who utilise the platform to make payments. This year, Cellulant raised $47.5 million from a collection of investors that included Satya Capital, TPG Growth, Endeavour Catalyst, and the Rise Fund.

- Tala, a mobile technology company that’s providing access to credit by putting mobile credit services into the hands of consumers, is operational in several countries in Africa and outside Africa. The company leverages an android app that collects data from each consumer, determines their credit score, and disburses a loan in <10 minutes. So far, the company has disbursed over a million dollars to individuals in East Africa and outside Africa.

- Numida, a digital financial services company situated in Uganda, won the Kampala Seedstar World Competition in 2017. The company boasts of a 99 percent repayment rate and has since disbursed about 190 loans to 135 Ugandan SMEs. Other than providing small unsecured loans to small businesses, the firm helps these businesses digitise their financial records through the Numida app. Through the Numida app, Numida can assess a client’s creditworthiness and then issues an appropriately sized unsecured loan.

Potential of using Fintech in Africa

![]() Africa is an immense continent with different economies supporting a total population of about 1 billion individuals residing in 54 sovereign countries. Surprisingly, only about 17 percent of the entire African population is banked. With nearly 80 percent of the total population still unbanked (and up to 95 million unbanked adults in Sub-Saharan Africa alone), Africa offers a unique breeding ground for the development of the fintech industry. A significant underbanked population ensures that fintech will most likely be an enabler of financial inclusion.

Africa is an immense continent with different economies supporting a total population of about 1 billion individuals residing in 54 sovereign countries. Surprisingly, only about 17 percent of the entire African population is banked. With nearly 80 percent of the total population still unbanked (and up to 95 million unbanked adults in Sub-Saharan Africa alone), Africa offers a unique breeding ground for the development of the fintech industry. A significant underbanked population ensures that fintech will most likely be an enabler of financial inclusion.

Innovation takes time and is often a collection of economies and nations that have the financial capability to invest, research, and develop on a broader scale. African nations, not having the same capabilities as developed nations, are provided with a unique opportunity that they can leverage. They can ‘jump’ inferior and redundant stages of technology advancement and go straight to adopting innovations. For example, currently, millions of Africans are in possession of mobile phone devices without ever going through the hassle of owning a landline at all. A phase that already-developed nations could not have skipped.

Technology is a crucial driver of businesses and entrepreneurship today. Due to this, financial procedures have been developing extremely fast, and there is an immense transformation in many aspects of financial processes. The Internet penetration rate in Africa recently stood at around 35.2 percent while the mobile penetration rate in the continent stands at 44 percent. Out of these two, Kenya emerges as the strongest African country, as it has an internet penetration rate of 85 percent and a mobile penetration rate of 95.1 percent.

According to GSMA, mobile money accounts in Africa have surpassed traditional bank accounts. Mobile money accounts have been on the rise, with statistics showing a steady growth in numbers from 0.2 million to 277 million between 2007 and 2016. The number of active bank accounts in Africa was 178 million as of December 2015. This huge difference in numbers indicates the potential that Africa offers to fintech startups focused on providing payment solutions. Technology innovation coupled with increasing Internet and mobile penetration rates have made the growth of African fintech companies a possibility. Subsequently, this has substantially increased investor interest in the sector even further.

Africa Welcoming Innovation

The fintech revolution in Africa is not a PR stunt. Fintech companies are attracting a previously unbanked population while at the same time retaining already existing traditional bank customers. Digitisation is helping financial institutions deliver digital financial products and services to a greater number of customers across the continent.

Increased dependence on these innovative fintech companies is projected to reduce demand for bank services. Subsequently, this could lead to bank branches shut down, with only a few remaining as destinations for problem resolution, advice, etc. For example, Kenya’s M-Pesa mobile payment services have made it possible for P2P mobile payments to be made both locally and internationally.

These startups are redefining the industry’s perception of what it means to be called a bank. Not only do they offer bank-like services, but they also avail loans, process financial transactions, and innovate much faster than banks.

Africa is hopping onto the fintech bandwagon, learning from the experiences of developed economies such as Asia, America, and Europe, and even leapfrogging past unnecessary steps, straight to modern innovation.

This guest post was contributed by Paweł Tomczyk, founder of the blockchain-focused content marketing agency Cyberius.

Ethereum is still the king of NFTs.

Despite surging interest in Bitcoin Ordinals and Solana’s memecoin-fueled NFT renaissance, Ethereum remains the chain of choice for high-value NFT collections and deep liquidity. But if you’re still using OpenSea as your go-to Ethereum NFT marketplace, you’re missing the bigger picture.

Magic Eden has quietly grown into the most active and user-friendly Ethereum NFT marketplace.

With a smooth UI, aggressive cross-chain integration, and a growing number of partnerships with top Ethereum collections, Magic Eden has emerged as the number one choice for collectors and creators alike.

This is especially relevant to Africa’s rising Web3 talent and crypto-savvy user base. As NFT adoption spreads across the continent, from digital art in Nairobi to music NFTs in Lagos, users are looking for marketplaces that offer real discoverability, cheaper transaction costs, and wider exposure. Magic Eden fits the bill.

TL;DR

- Magic Eden has become the leading Ethereum NFT marketplace, surpassing OpenSea in user experience and aggregated listings.

- It offers the largest selection of Ethereum NFTs by aggregating listings from other platforms, including OpenSea.

- With cross-chain functionality, low fees, and a clean UI, it’s especially valuable for African creators and collectors entering the NFT space.

- Its community-driven approach and growing partnerships make it a top destination for Ethereum NFTs, globally and across Africa.

Why Magic Eden Stands Out in the Ethereum NFT Landscape

Magic Eden didn’t just show up on Ethereum: it made a statement.

While legacy marketplaces rested on their early-mover status, Magic Eden built a better experience from the ground up. Its rapid rise in the Ethereum NFT space comes down to a combination of smart technical integrations, creator-first tools, and a user interface that just works.

Here’s what sets it apart:

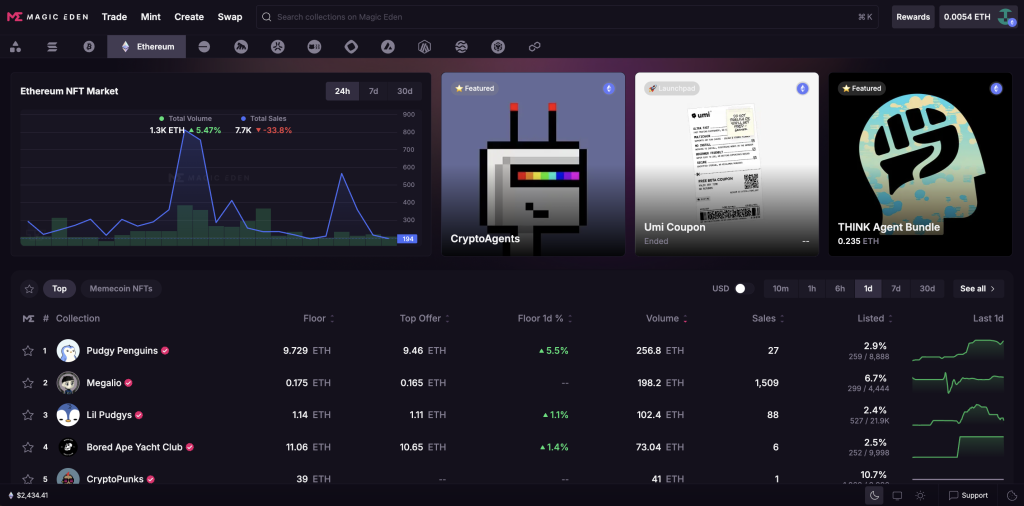

Largest Aggregated Selection of Ethereum NFTs

Magic Eden aggregates listings from multiple Ethereum NFT marketplaces, including OpenSea, but not the other way around. That means you’ll find more collections on Magic Eden than anywhere else, and often better prices.

This is crucial in a maturing market. Rather than chasing hype, Ethereum collectors today are looking for value, rarity, and provenance. Aggregation allows for better price discovery, more liquidity, and a one-stop-shop browsing experience that cuts through the noise.

Whether you’re looking for Trump’s NFT collection (on Polygon), the infamous Bored Ape Yacht Club NFTs, the cute Pudgy Penguins NFTs, or

It’s Actually Cross-Chain (and It Works)

Unlike other Ethereum NFT marketplaces that only claim to be cross-chain, Magic Eden has fully integrated support for Bitcoin, Polygon, and 10+ other chains, too. And this isn’t just window dressing.

You can use one wallet to trade across chains, and the UI stays consistent no matter which chain you’re exploring.

For African creators and collectors navigating different ecosystems, from Polygon’s low-gas minting to Bitcoin Ordinals, this is a game-changer. You don’t have to switch platforms or lose visibility because of your chain of choice.

Clean Interface, Low Fees, Easy Onboarding

Magic Eden’s Ethereum marketplace is built with usability in mind. The onboarding process is simple, the search function is robust, and you don’t need to be a degen to find your way around.

For creators across Africa who are new to the Ethereum NFT space, this lowers the barrier to entry. Artists can focus on launching their work without worrying about poor UI, clunky listing flows, or high gas fees (Magic Eden lets you batch list and supports low-fee chains like Polygon and Solana as alternatives).

Backed by Real Partnerships and Community Culture

Magic Eden is also making smart moves in the culture and community department, something that matters more than most people think. It has secured official partnerships with Ethereum-native collections like Yuga Labs’ Otherside, and continues to collaborate with emerging creators globally.

It doesn’t feel corporate or extractive.

For African creators exploring global audiences, this positioning matters. Magic Eden feels closer to the community than peers like Blur or LooksRare, which cater mostly to high-volume traders and whales.

“Magic Eden is changing the game not just for collectors in the West, but for African creators looking for global exposure without compromising on ease of use. It’s the most creator-friendly Ethereum marketplace I’ve seen yet,” says Lucy Manzi, NFT Collector & Trader at Kotani Pay.

Ethereum Still Matters, Especially in Africa

While Bitcoin is growing fast as a transactional asset in Africa and Solana is seeing traction in mobile-first NFT experiences, Ethereum remains the most established ecosystem for digital collectibles.

From generative art to tokenized fashion, most of the Web3 projects making global headlines are still Ethereum-based.

As African creators and startups look to tap into international collector communities, being present on Ethereum (and on the right Ethereum marketplace) is key. Magic Eden provides visibility without compromise.

For African developers building NFT tools or for regional exchanges looking to integrate NFT support, Magic Eden’s open APIs and aggregated listings create opportunities for partnership and expansion without needing to start from scratch.

Final Thoughts

The Ethereum NFT market is no longer dominated by OpenSea. Magic Eden has taken the crown by doing what others wouldn’t: building across chains, simplifying the experience, and respecting creators.

For NFT creators and collectors, Magic Eden offers a practical, intuitive, and future-forward marketplace experience, whether you’re minting your first piece of digital art, flipping trending collections, or building a Web3 brand that spans borders.

In a continent where mobile-first adoption is high, cross-chain compatibility and low-gas minting options matter. Magic Eden delivers on both fronts while giving Ethereum NFTs the spotlight they deserve.

Whether you’re in Nairobi, Cape Town, Accra, or Abuja, if you’re playing in the NFT space, Magic Eden is worth your attention.

Cryptocurrencies have disrupted traditional financial systems in recent years, and Bitcoin profiled itself as the most famous crypto. It has already found its way to e-commerce and investment, but this crypto is also present in the world of online gaming. In this article, we will explore the growing influence of Bitcoin in the online gaming world.

Bitcoin and Online Casinos

Thanks to Bitcoin’s integration into online casinos, players and operators now have a vast range of possibilities. With the use of Bitcoin, online casinos create another level of advantage over traditional payment options. Most of all, if you perform transactions in Bitcoin, they will be quicker and more efficient.

You can deposit or withdraw the funds within seconds without the need for complex verification processes or intermediaries. This makes the gaming experience smoother and more seamless for any player. Additionally, Bitcoin offers a higher level of privacy and security. We have already experienced how much financial and personal information traditional payment methods require.

Nevertheless, unlike them, Bitcoin transactions are pseudonymous, which means they provide players with greater anonymity. This privacy feature particularly appeals to those who value their online security and wish to enjoy online gaming without revealing their identities. Integrating Bitcoin into online casinos has also resulted in innovative bonus structures and rewards.

Some Bitcoin casinos offer exclusive promotions and bonuses for players who use Bitcoin as their preferred payment method. The best Bitcoin casinos in the Philippines are safe to deposit at, according to this guide, and you can choose the one that appeals to you the most. That’s why more and more players turn to Bitcoin as their payment method, fostering its further adoption in the gaming industry.

Since Bitcoin is decentralized, transactions bypass the regular censorship and control that we can see involved with traditional payment methods. Thanks to this, players from regions with strict gambling regulations can participate in online gaming with fewer restrictions. Bitcoin-powered online casinos do not impose geographical limitations, opening their services to players worldwide.

Bitcoin and Esports Betting

Beyond online casinos, Bitcoin has made significant breakthroughs in esports betting. We could witness a skyrocketing rise of esports in recent years, which resulted in millions of enthusiasts and viewers worldwide. Thanks to Bitcoin’s integration into esports, players have a wider range of options to engage with their favorite games and gamers.

Esports, or competitive video gaming, has witnessed a meteoric rise in popularity, attracting millions of viewers and enthusiasts worldwide. Bitcoin’s integration into esports betting platforms has revolutionized how fans engage with their favorite games and players.

Bitcoin’s advantages, such as fast and secure transactions, align perfectly with the dynamic nature of esports betting. Users can easily deposit and withdraw funds, allowing for quick reactions to changing odds or game outcomes. Bitcoin’s decentralized nature also ensures that bettors from any location can participate, overcoming the obstacles of regional restrictions and currency exchange complications.

Moreover, Bitcoin’s integration into esports betting platforms has provided players with increased transparency and fairness. The technology behind Bitcoin, blockchain, allows for unalterable and auditable records of transactions, ensuring that betting outcomes are tamper-proof.

This transparency has fostered greater trust among players, operators, and regulators, further fueling the growth of Bitcoin-powered esports betting.

Bitcoin and In-Game Purchases

As the gaming industry evolves, it has also opened innovative ways for gamers to enhance their gaming experience. With the involvement of Bitcoin, players can use it for in-game purchases. Nowadays, many popular online games support cryptocurrencies for item purchases, upgrades, or other enhancements.

Since crypto transactions are more seamless, Bitcoin has become a better alternative compared to traditional in-game payment methods. Game developers have also benefited from introducing Bitcoin as a payment option. Now they can offer a more convenient way of purchasing in-game items, transaction fees are lower, and processing times have become faster.

Moreover, you, as a player, don’t need to disclose any sensitive information anymore. That way, Bitcoin usage in gaming reduces the risk of potential data breaches. The adoption of Bitcoin in in-game purchases has also opened up new possibilities for cross-platform transactions.

As Bitcoin operates globally, players can easily trade or transfer in-game assets across different games or platforms, fostering a vibrant secondary market for virtual goods. This flexibility enhances player engagement and allows for a more interconnected gaming experience.

The integration of Bitcoin into in-game purchases has also paved the way for blockchain-based gaming ecosystems. Some game developers have embraced blockchain technology to create decentralized gaming platforms where players truly own their in-game assets through blockchain-based tokens. This ownership empowers players and introduces concepts of shortage and value to virtual items.

Benefits of Using Bitcoin in Online Gaming

Players can enjoy multiple benefits from using Bitcoin in online gaming. The most obvious one is that traditional payment methods cannot match the level of Bitcoin’s security and anonymity. Due to cryptos’ decentralized nature, you don’t need to disclose your sensitive data. If you want to get started in the gaming world easily and quickly, there’s no more attractive option than Bitcoin.

Transactions are completed within seconds, and they are cheaper in terms of fees compared to other popular methods. Since Bitcoin has become more popular in the online gaming industry, gaming platforms recognized its benefits.

Therefore, they introduced it as a payment method, and nowadays, the world’s most popular online gaming platforms accept Bitcoin, including Steam, Xbox Live, and PlayStation Network.

Security Considerations When Using Bitcoin in Gaming

While Bitcoin offers many benefits for online gaming, such as fast and secure transactions, there are also some security considerations to keep in mind. Performing online financial transactions always brings a high risk of potential hacking and theft of Bitcoin wallets. That’s why you should use a secure and reputable digital wallet and keep your private keys safe and inaccessible to unauthorized persons.

Also, online gaming platforms that you use should have strong security features established to keep your financial and personal information away from the eyes of unauthorized third parties.

Conclusion

Bitcoin’s rise in online gaming has brought many benefits for all entities in this growing industry. From online casinos to esports betting and in-game purchases, Bitcoin’s unique characteristics have reshaped the gaming landscape, offering increased speed, privacy, security, and global accessibility. It shouldn’t take too long before cryptocurrencies gain mainstream acceptance since they are continuously evolving.

That’s why we believe the Bitcoin integration in the online gaming industry will continue. Ultimately, it should unlock new ways of innovation and interaction for gaming fans worldwide, leading to limitless possibilities for the future of online gaming.

Magic Eden Has Quietly Become the Best Ethereum NFT Marketplace

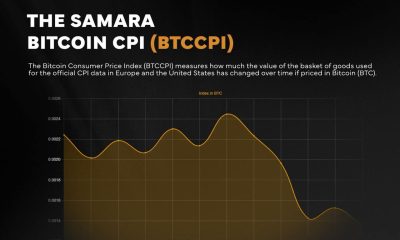

Samara Asset Group Launches Bitcoin CPI (BTCCPI)

Introducing Noones – Africa’s P2P Super App

Why Crypto’s Leading the Way in Africa’s Evolving Finance Landscape

The Rise of Bitcoin in the Online Gaming World

Unlock the Thrills of NHL Crypto Betting and Live Streaming

Understanding the Impact of Cryptocurrency Volatility on NBA Betting Markets

The Future of Crypto College Football Betting: Trends and Predictions

How Mobile Apps are Changing Sports Betting