Features

3 Ways Governments Could Use Blockchain Technology to Oppress its Citizens

The blockchain has many applications for the public sector that can improve the quality of government services, safeguard property rights, prevent fraud, and cut red tape while improving transparency. However, what is not often discussed, is that malicious governments could also use blockchain technology to oppress its citizens.

This article highlights how governments could potentially misuse the blockchain to reduce the individual liberties of its citizens and suppress those with opposing views.

When a Sovereign Digital Currency Means Tracking All Financial Transactions

Blockchain-based decentralised digital currencies have the potential to enable economic, political and social freedom. Conversely, the emergence of sovereign centralized “cryptocurrencies” – issued by central banks – contradicts everything that bitcoin and the blockchain stand for and hoped to fix.

The main goal of cryptocurrencies was to decentralize power, not to boost existing authorities. With centralized state-run blockchains, power is heavily concentrated as governments maintain control over the entire network.

The main goal of cryptocurrencies was to decentralize power, not to boost existing authorities. With centralized state-run blockchains, power is heavily concentrated as governments maintain control over the entire network.

Government-controlled cryptocurrencies could impose dangerous limitations on citizen’s civil freedoms, including pervasive anti-privacy measures.

By being able to track every single financial transaction, citizens would lose their financial sovereignty and the personal freedom that comes with spending one’s money on whatever a citizen wants.

Having every single transaction tracked would inevitably lead to mass financial data collection to determine behavioural and spending patterns of each individual in the country, which could be used against them, should they become at odds with the government or someone with close government ties.

When Blockchain-based Digital Identities Are Used to Track Digital Footprints

One of the most impactful developments in the blockchain industry has been the advancement of secure digital identities. Identification is needed for everything from voting to health care. For the over one billion people worldwide who do not have a legal form of identity, digital identities can provide a much-needed solution.

Digital identities can be stored on a blockchain, which can then be used to handle information such as a patient’s medical records, which can be easily and safely accessed by a health care provider when they are seeking care.

However, if a malicious government has full control of the digital ID system and all its citizens’ data, it could use this to track each citizen’s digital footprints. For example, if the social media accounts, financial services, mobile payment firms accounts of citizens are bound to their digital identity, the government could very easily track individuals’ movements in real-time.

This already happens to a degree in countries like the U.S and U.K. as we learned from Edward Snowden’s NSA leaks. Every day, intelligence agencies collect hundreds of millions of emails, texts, and phone calls and can collect and sift through billions more. The surveillance technology for tracking and identifying people is booming as is governments’ appetite for it. Add in the current digital tracking systems with facial recognition software and digital identities, and this endangers citizen’s right to privacy.

Blockchain-based digital identity systems thus need to be implemented with care and the oversight of the network should not be limited to the government as the potential for misuse is huge.

When Digital Identities Are Used to Create a Social Credit Scoring System

Credit scores dictate a person’s involvement in the financial system, including loan or mortgage approvals, interest rates, and insurance rates. It can impact someone’s ability to rent an apartment or secure a credit card, for example.

China’s latest surveillance efforts include a social credit system that aims to rate each citizen’s social value according to their actions.

Drawing data from government agencies, court verdicts, and even mobile payment firms, the scheme assigns each person an individual score. Failure to repay debts or smoked on a train, you could land on a blacklist posted on a public website. The plan is to rate citizens by their financial and legal histories, their online behaviour, education records, and employment activities.

If such an oppressive social credit scoring system is implemented and interlinked with blockchain technology, the data stored on the system would become immutable and easily shareable with permissioned third parties, such as corporations, who could, in turn, limit low-ranking individuals’ ability to live freely even further.

Such a system could be used by governments to oppress its citizens especially those seen as having a lesser value or those that threaten its power. The blockchain could potentially amplify the oppressive nature of such a social credit scoring system.

Keep Your Leaders in Check

While the blockchain was created to decentralize power, the unfortunate reality is that as the technology has evolved, there are now ways it could be used to make oppressive governments more powerful.

Hence, it is important to stay mindful of how the blockchain can be misused when you hear of your government implementing a new blockchain initiative and to speak up if the initiative could go turn into a tool of oppression.

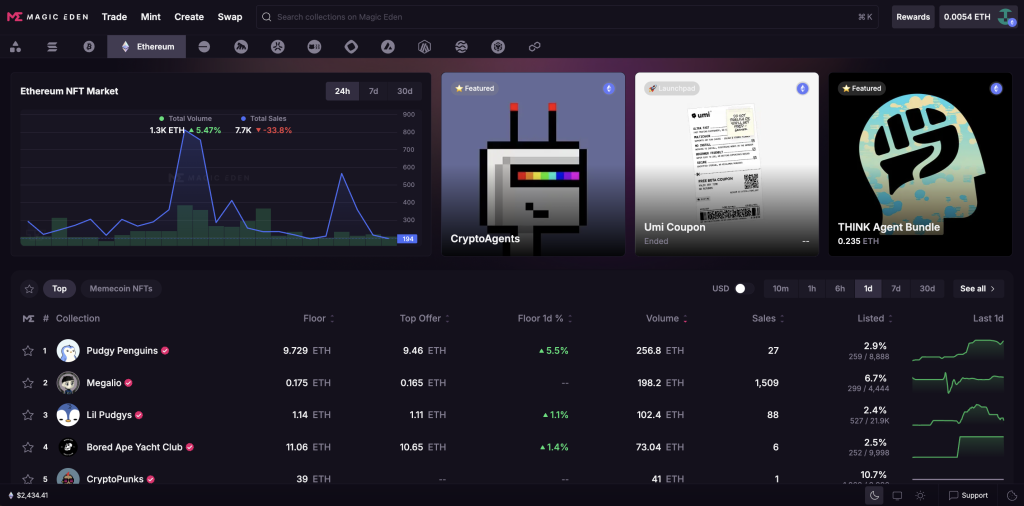

Ethereum is still the king of NFTs.

Despite surging interest in Bitcoin Ordinals and Solana’s memecoin-fueled NFT renaissance, Ethereum remains the chain of choice for high-value NFT collections and deep liquidity. But if you’re still using OpenSea as your go-to Ethereum NFT marketplace, you’re missing the bigger picture.

Magic Eden has quietly grown into the most active and user-friendly Ethereum NFT marketplace.

With a smooth UI, aggressive cross-chain integration, and a growing number of partnerships with top Ethereum collections, Magic Eden has emerged as the number one choice for collectors and creators alike.

This is especially relevant to Africa’s rising Web3 talent and crypto-savvy user base. As NFT adoption spreads across the continent, from digital art in Nairobi to music NFTs in Lagos, users are looking for marketplaces that offer real discoverability, cheaper transaction costs, and wider exposure. Magic Eden fits the bill.

TL;DR

- Magic Eden has become the leading Ethereum NFT marketplace, surpassing OpenSea in user experience and aggregated listings.

- It offers the largest selection of Ethereum NFTs by aggregating listings from other platforms, including OpenSea.

- With cross-chain functionality, low fees, and a clean UI, it’s especially valuable for African creators and collectors entering the NFT space.

- Its community-driven approach and growing partnerships make it a top destination for Ethereum NFTs, globally and across Africa.

Why Magic Eden Stands Out in the Ethereum NFT Landscape

Magic Eden didn’t just show up on Ethereum: it made a statement.

While legacy marketplaces rested on their early-mover status, Magic Eden built a better experience from the ground up. Its rapid rise in the Ethereum NFT space comes down to a combination of smart technical integrations, creator-first tools, and a user interface that just works.

Here’s what sets it apart:

Largest Aggregated Selection of Ethereum NFTs

Magic Eden aggregates listings from multiple Ethereum NFT marketplaces, including OpenSea, but not the other way around. That means you’ll find more collections on Magic Eden than anywhere else, and often better prices.

This is crucial in a maturing market. Rather than chasing hype, Ethereum collectors today are looking for value, rarity, and provenance. Aggregation allows for better price discovery, more liquidity, and a one-stop-shop browsing experience that cuts through the noise.

Whether you’re looking for Trump’s NFT collection (on Polygon), the infamous Bored Ape Yacht Club NFTs, the cute Pudgy Penguins NFTs, or

It’s Actually Cross-Chain (and It Works)

Unlike other Ethereum NFT marketplaces that only claim to be cross-chain, Magic Eden has fully integrated support for Bitcoin, Polygon, and 10+ other chains, too. And this isn’t just window dressing.

You can use one wallet to trade across chains, and the UI stays consistent no matter which chain you’re exploring.

For African creators and collectors navigating different ecosystems, from Polygon’s low-gas minting to Bitcoin Ordinals, this is a game-changer. You don’t have to switch platforms or lose visibility because of your chain of choice.

Clean Interface, Low Fees, Easy Onboarding

Magic Eden’s Ethereum marketplace is built with usability in mind. The onboarding process is simple, the search function is robust, and you don’t need to be a degen to find your way around.

For creators across Africa who are new to the Ethereum NFT space, this lowers the barrier to entry. Artists can focus on launching their work without worrying about poor UI, clunky listing flows, or high gas fees (Magic Eden lets you batch list and supports low-fee chains like Polygon and Solana as alternatives).

Backed by Real Partnerships and Community Culture

Magic Eden is also making smart moves in the culture and community department, something that matters more than most people think. It has secured official partnerships with Ethereum-native collections like Yuga Labs’ Otherside, and continues to collaborate with emerging creators globally.

It doesn’t feel corporate or extractive.

For African creators exploring global audiences, this positioning matters. Magic Eden feels closer to the community than peers like Blur or LooksRare, which cater mostly to high-volume traders and whales.

“Magic Eden is changing the game not just for collectors in the West, but for African creators looking for global exposure without compromising on ease of use. It’s the most creator-friendly Ethereum marketplace I’ve seen yet,” says Lucy Manzi, NFT Collector & Trader at Kotani Pay.

Ethereum Still Matters, Especially in Africa

While Bitcoin is growing fast as a transactional asset in Africa and Solana is seeing traction in mobile-first NFT experiences, Ethereum remains the most established ecosystem for digital collectibles.

From generative art to tokenized fashion, most of the Web3 projects making global headlines are still Ethereum-based.

As African creators and startups look to tap into international collector communities, being present on Ethereum (and on the right Ethereum marketplace) is key. Magic Eden provides visibility without compromise.

For African developers building NFT tools or for regional exchanges looking to integrate NFT support, Magic Eden’s open APIs and aggregated listings create opportunities for partnership and expansion without needing to start from scratch.

Final Thoughts

The Ethereum NFT market is no longer dominated by OpenSea. Magic Eden has taken the crown by doing what others wouldn’t: building across chains, simplifying the experience, and respecting creators.

For NFT creators and collectors, Magic Eden offers a practical, intuitive, and future-forward marketplace experience, whether you’re minting your first piece of digital art, flipping trending collections, or building a Web3 brand that spans borders.

In a continent where mobile-first adoption is high, cross-chain compatibility and low-gas minting options matter. Magic Eden delivers on both fronts while giving Ethereum NFTs the spotlight they deserve.

Whether you’re in Nairobi, Cape Town, Accra, or Abuja, if you’re playing in the NFT space, Magic Eden is worth your attention.

Cryptocurrencies have disrupted traditional financial systems in recent years, and Bitcoin profiled itself as the most famous crypto. It has already found its way to e-commerce and investment, but this crypto is also present in the world of online gaming. In this article, we will explore the growing influence of Bitcoin in the online gaming world.

Bitcoin and Online Casinos

Thanks to Bitcoin’s integration into online casinos, players and operators now have a vast range of possibilities. With the use of Bitcoin, online casinos create another level of advantage over traditional payment options. Most of all, if you perform transactions in Bitcoin, they will be quicker and more efficient.

You can deposit or withdraw the funds within seconds without the need for complex verification processes or intermediaries. This makes the gaming experience smoother and more seamless for any player. Additionally, Bitcoin offers a higher level of privacy and security. We have already experienced how much financial and personal information traditional payment methods require.

Nevertheless, unlike them, Bitcoin transactions are pseudonymous, which means they provide players with greater anonymity. This privacy feature particularly appeals to those who value their online security and wish to enjoy online gaming without revealing their identities. Integrating Bitcoin into online casinos has also resulted in innovative bonus structures and rewards.

Some Bitcoin casinos offer exclusive promotions and bonuses for players who use Bitcoin as their preferred payment method. The best Bitcoin casinos in the Philippines are safe to deposit at, according to this guide, and you can choose the one that appeals to you the most. That’s why more and more players turn to Bitcoin as their payment method, fostering its further adoption in the gaming industry.

Since Bitcoin is decentralized, transactions bypass the regular censorship and control that we can see involved with traditional payment methods. Thanks to this, players from regions with strict gambling regulations can participate in online gaming with fewer restrictions. Bitcoin-powered online casinos do not impose geographical limitations, opening their services to players worldwide.

Bitcoin and Esports Betting

Beyond online casinos, Bitcoin has made significant breakthroughs in esports betting. We could witness a skyrocketing rise of esports in recent years, which resulted in millions of enthusiasts and viewers worldwide. Thanks to Bitcoin’s integration into esports, players have a wider range of options to engage with their favorite games and gamers.

Esports, or competitive video gaming, has witnessed a meteoric rise in popularity, attracting millions of viewers and enthusiasts worldwide. Bitcoin’s integration into esports betting platforms has revolutionized how fans engage with their favorite games and players.

Bitcoin’s advantages, such as fast and secure transactions, align perfectly with the dynamic nature of esports betting. Users can easily deposit and withdraw funds, allowing for quick reactions to changing odds or game outcomes. Bitcoin’s decentralized nature also ensures that bettors from any location can participate, overcoming the obstacles of regional restrictions and currency exchange complications.

Moreover, Bitcoin’s integration into esports betting platforms has provided players with increased transparency and fairness. The technology behind Bitcoin, blockchain, allows for unalterable and auditable records of transactions, ensuring that betting outcomes are tamper-proof.

This transparency has fostered greater trust among players, operators, and regulators, further fueling the growth of Bitcoin-powered esports betting.

Bitcoin and In-Game Purchases

As the gaming industry evolves, it has also opened innovative ways for gamers to enhance their gaming experience. With the involvement of Bitcoin, players can use it for in-game purchases. Nowadays, many popular online games support cryptocurrencies for item purchases, upgrades, or other enhancements.

Since crypto transactions are more seamless, Bitcoin has become a better alternative compared to traditional in-game payment methods. Game developers have also benefited from introducing Bitcoin as a payment option. Now they can offer a more convenient way of purchasing in-game items, transaction fees are lower, and processing times have become faster.

Moreover, you, as a player, don’t need to disclose any sensitive information anymore. That way, Bitcoin usage in gaming reduces the risk of potential data breaches. The adoption of Bitcoin in in-game purchases has also opened up new possibilities for cross-platform transactions.

As Bitcoin operates globally, players can easily trade or transfer in-game assets across different games or platforms, fostering a vibrant secondary market for virtual goods. This flexibility enhances player engagement and allows for a more interconnected gaming experience.

The integration of Bitcoin into in-game purchases has also paved the way for blockchain-based gaming ecosystems. Some game developers have embraced blockchain technology to create decentralized gaming platforms where players truly own their in-game assets through blockchain-based tokens. This ownership empowers players and introduces concepts of shortage and value to virtual items.

Benefits of Using Bitcoin in Online Gaming

Players can enjoy multiple benefits from using Bitcoin in online gaming. The most obvious one is that traditional payment methods cannot match the level of Bitcoin’s security and anonymity. Due to cryptos’ decentralized nature, you don’t need to disclose your sensitive data. If you want to get started in the gaming world easily and quickly, there’s no more attractive option than Bitcoin.

Transactions are completed within seconds, and they are cheaper in terms of fees compared to other popular methods. Since Bitcoin has become more popular in the online gaming industry, gaming platforms recognized its benefits.

Therefore, they introduced it as a payment method, and nowadays, the world’s most popular online gaming platforms accept Bitcoin, including Steam, Xbox Live, and PlayStation Network.

Security Considerations When Using Bitcoin in Gaming

While Bitcoin offers many benefits for online gaming, such as fast and secure transactions, there are also some security considerations to keep in mind. Performing online financial transactions always brings a high risk of potential hacking and theft of Bitcoin wallets. That’s why you should use a secure and reputable digital wallet and keep your private keys safe and inaccessible to unauthorized persons.

Also, online gaming platforms that you use should have strong security features established to keep your financial and personal information away from the eyes of unauthorized third parties.

Conclusion

Bitcoin’s rise in online gaming has brought many benefits for all entities in this growing industry. From online casinos to esports betting and in-game purchases, Bitcoin’s unique characteristics have reshaped the gaming landscape, offering increased speed, privacy, security, and global accessibility. It shouldn’t take too long before cryptocurrencies gain mainstream acceptance since they are continuously evolving.

That’s why we believe the Bitcoin integration in the online gaming industry will continue. Ultimately, it should unlock new ways of innovation and interaction for gaming fans worldwide, leading to limitless possibilities for the future of online gaming.

Magic Eden Has Quietly Become the Best Ethereum NFT Marketplace

Samara Asset Group Launches Bitcoin CPI (BTCCPI)

Introducing Noones – Africa’s P2P Super App

Why Crypto’s Leading the Way in Africa’s Evolving Finance Landscape

The Rise of Bitcoin in the Online Gaming World

Unlock the Thrills of NHL Crypto Betting and Live Streaming

Understanding the Impact of Cryptocurrency Volatility on NBA Betting Markets

The Future of Crypto College Football Betting: Trends and Predictions

How Mobile Apps are Changing Sports Betting